Florida Lady Bird Deed for Mortgaged Property: Preserve Equity & Control. Get a Florida Lady Bird Deed to keep your Mortgaged Property, Preserve Equity & Control.

Purpose & Benefits of a Florida Lady Bird Deed for Mortgaged Property: Preserve Equity & Control

The Florida Lady Bird Deed for Mortgaged Property: Preserve Equity & Control provides homeowners an effective way to transfer real estate upon death without the delay & expense of probate. By using this deed, you can retain full ownership rights use, lease, mortgage or sell during your lifetime. It allows you to designate one or more beneficiaries who will automatically receive title to the property at your passing. This approach safeguards your home equity from being tied up in court proceedings, while you continue to make mortgage payments & enjoy tax benefits uninterrupted.

In addition, this deed offers exceptional flexibility because it operates outside of a traditional trust structure. You avoid trustee fees & the complexities of ongoing trust management. Beneficiaries gain immediate ownership without the hassle of probate, which can save thousands in court costs & legal fees. Creditors cannot attack the beneficiary’s interest until after your death, so your mortgage lender retains its security interest until the debt is paid. By integrating a Lady Bird Deed into your estate plan, you maximize control over your property while ensuring a seamless transfer later on.

| Feature | Benefit |

|---|---|

| Retained Control | Use & sell property during lifetime |

| Probate Avoidance | Immediate transfer at death |

| Creditor Protection | Only binds after owner’s death |

“A properly drafted Lady Bird Deed can save heirs significant time & money by bypassing probate entirely.” – Deven Daugherty

How to Create & File a Florida Lady Bird Deed for Mortgaged Property: Preserve Equity & Control

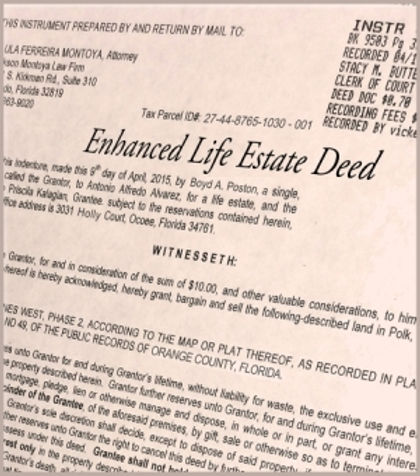

Drafting a Florida Lady Bird Deed for Mortgaged Property: Preserve Equity & Control requires precise language to ensure validity under Florida law. Begin with a standard quitclaim deed form, then add specific clauses reserving lifetime rights. These reserved rights must include the ability to sell, lease, mortgage or otherwise manage the property without beneficiary consent. Identify current mortgage status & property description clearly. It’s crucial to list grantor, grantee & contingent remaindermen with full legal names & addresses to avoid ambiguities.

- Consult a Florida real estate attorney to draft or review the deed template.

- Ensure the deed language complies with Florida Statute 732.7055 for enhanced life estate instruments.

- Include a clear description of reserved rights & remaindermen beneficiaries.

- Obtain the grantor’s notarized signature & two witnesses if required by county rules.

- Record the deed at the county clerk’s office where the property is located.

Once recorded, the deed becomes public record, so confirm proper indexing by verifying the document number with the clerk. Keep a certified copy in your safe or with your estate planning file. Notify beneficiaries of the recorded deed, so they understand the timeline & their future interest. Finally, review your mortgage terms to ensure there are no prohibitions on transferring any beneficial interest, although a life estate reservation typically does not trigger a due-on-sale clause.

Impact on Original Mortgage & Lender Considerations

When you execute a Florida Lady Bird Deed for Mortgaged Property: Preserve Equity & Control, your existing mortgage remains intact. Lenders usually cannot exercise a due-on-sale clause because the transfer reserves your life estate rights. This means you continue making payments under the original loan terms. The deed does not absolve you from liability; you remain responsible for timely payments, taxes, insurance & property maintenance. Beneficiaries have no obligation to repay the loan while you’re alive.

| Lender Concern | Resolution |

|---|---|

| Due-on-Sale Clause | Life estate reservation preserves lender’s interest |

| Loan Transfer | No transfer until owner’s death |

| Insurance Requirements | Owner maintains insurance coverage |

Before filing, inform your lender of the planned Lady Bird Deed to avoid surprises. Although Florida law protects these deeds, some lenders prefer notification. Provide a copy of the draft deed & discuss its impact on your mortgage covenant. Many mortgage servicers recognize this tool as a benign estate planning measure & permit it without alteration. Document the lender’s approval or objection in writing. Keep records of correspondence in case of future disputes or conveyance questions.

Comparing a Lady Bird Deed to Other Estate Planning Tools

Different estate planning devices serve distinct goals, & a Florida Lady Bird Deed for Mortgaged Property: Preserve Equity & Control excels at real estate transfer without probate but does not replace a will or trust fully. A revocable living trust provides control during lifetime & at death, yet it requires funding, trustee duties & higher setup costs. A simple will may name beneficiaries but still subjects your property to probate, causing delays & public record. Each instrument carries tax implications & administrative burdens.

- Revocable Living Trust: Offers comprehensive asset management but requires transferring all assets into the trust & ongoing reviews.

- Simple Will: Inexpensive setup but subjects property to probate; not ideal for high-value real estate.

- Lady Bird Deed: Specialized for Florida real estate; immediate transfer at death with no probate; minimal ongoing administration.

- Transfer-on-Death Deed (outside Florida): Similar benefits but only in states that accept this device; local statutes vary.

By integrating a Lady Bird Deed with other estate planning, you create a hybrid strategy. Use the deed for Florida properties, maintain a trust for non‐real‐estate assets, & keep a will to capture any overlooked items. Regular reviews ensure the package aligns with changes in family circumstances or law updates. Coordinating with your estate planning attorney will streamline documents, clarify beneficiary designations, & reduce tax exposure.

Common Pitfalls in Florida Lady Bird Deed for Mortgaged Property: Preserve Equity & Control & How to Avoid Them

Errors in drafting or recording a Florida Lady Bird Deed for Mortgaged Property: Preserve Equity & Control can invalidate the instrument or trigger unintended legal consequences. One frequent mistake is omitting the explicit reservation of life estate rights. Without this language, the deed may convert into an outright transfer, potentially violating mortgage covenants. Another risk is misidentifying beneficiaries or failing to update the deed after major life events like divorce, remarriage or birth of a new heir.

| Pitfall | Prevention |

|---|---|

| Improper Language | Use statutory approved wording |

| Wrong Beneficiary Identification | Include full legal names & relationships |

| Failure to Record | Verify county clerk acceptance & indexing |

| Ignored Mortgage Terms | Consult lender before recording |

Periodic reviews are crucial: revisit your deed whenever you move, refinance or take out a home equity line of credit. Confirm the recorded deed remains indexed correctly by pulling a clerk’s office title report. Consult your estate planning attorney to revise the deed after beneficiary death or if tax laws change. By proactively monitoring & maintaining accurate documentation, you ensure your equity & control provisions remain intact.

Legal & Tax Implications of Executing a Florida Lady Bird Deed for Mortgaged Property: Preserve Equity & Control

Implementing a Florida Lady Bird Deed for Mortgaged Property: Preserve Equity & Control carries specific legal & tax consequences you must understand. Legally, the deed qualifies as an enhanced life estate under Florida statutes, so it will override conflicting provisions in your will regarding the same property. Beneficiaries receive a stepped-up basis at your death, minimizing capital gains tax if they later sell. You retain all tax deductions, exemptions & homestead benefits until death.

- Homestead Exemption: Maintained by the grantor throughout lifetime.

- Capital Gains: Stepped-up basis for beneficiaries reduces taxable gains on sale after transfer.

- Gift Tax: No gift tax reported since the transfer occurs at death, not during lifetime.

- Medicaid Planning: Property still counts as an asset until the grantor’s passing, so it may not provide asset protection for long-term care benefits.

Consult both an estate planning attorney & a tax advisor to review implications unique to your situation. Document your intentions clearly to reduce family disputes. Keep detailed records of your residency & property improvements to defend homestead & basis claims. Understanding these nuances ensures you preserve maximum equity & control from execution to ultimate transfer.

My Personal Experience with Florida Lady Bird Deed for Mortgaged Property: Preserve Equity & Control

I first used a Lady Bird Deed for my own mortgaged home when I wanted to keep making mortgage payments & claiming homestead benefits, while also ensuring my children would inherit the property directly without probate. I worked closely with a local attorney who drafted precise life estate language, reserved all my rights & named my kids as contingent remaindermen. After recording, I confirmed the deed’s indexing & informed my lender. This tool gave me peace of mind knowing I controlled the house until my final day & that my family avoided lengthy court delays.

FAQ

What is a Lady Bird Deed & how does it work in Florida?

A Lady Bird Deed is an enhanced life estate deed that lets a property owner retain full control use, mortgage, sell during life while designating beneficiaries to inherit at death without probate. It’s governed by Florida Statute 732.7055, ensuring the deed is valid if properly drafted & recorded.

Will the original mortgage be called due when I record this deed?

No. The deed reserves the grantor’s life estate rights, which means the mortgage lender’s security interest remains valid after recording. The due-on-sale clause is generally not triggered by this type of transfer.

Can I change or revoke a Lady Bird Deed once it’s recorded?

Yes. You can amend or revoke it at any time through a recorded revocation deed or by executing a new Lady Bird Deed with updated provisions. Always record changes in the same county clerk’s office.

How does this deed affect Medicaid eligibility?

The property remains countable for Medicaid long-term care eligibility until the owner’s death. The enhanced life estate does not offer asset protection like certain irrevocable trusts.

Conclusion

Adopting a Florida Lady Bird Deed for Mortgaged Property: Preserve Equity & Control can be one of the most strategic decisions for Florida homeowners seeking to maintain lifetime authority over their real estate while guaranteeing a streamlined transfer to heirs. By leveraging this enhanced life estate, you ensure that your mortgage terms continue uninterrupted, that you benefit from homestead exemptions & tax deductions, & that your beneficiaries receive a stepped-up basis upon inheritance. Proper drafting & filing are critical: always work with a qualified estate planning attorney to confirm statutory compliance, address lender requirements & ward off common drafting errors.

Alternating between tables & lists in your research can help clarify benefits, steps & pitfalls, making it easier to share with family or advisors. Following the step-by-step guidelines presented here, you’ll preserve equity, avoid probate delays & maintain control of your property throughout your lifetime. Whether you’re nearing retirement or simply planning ahead, integrating a Lady Bird Deed into your estate plan offers peace of mind & financial efficiency. Consult legal & tax professionals to tailor this tool to your goals, keep your documentation current, & protect your legacy.